Compare Point of Sale (POS) Fee Structures: Interchange Plus Vs. Flat Rate Processing

POS pricing can make your head spin, but it doesn't need to. We're here to help. Learn the need-to-know terms and how to compare POS fee structures.

Point of sale (POS) processing fee structures aren’t the most exciting topic, but they’re unavoidable if you want to transact with debit and credit cards. Plus, it’s critical to small business success to understand them so you can make the right decision for your people and your profits!

Below are need-to-know terms when it comes to POS fee structures as well as a definitive comparison between Interchange Plus and Flat Rate processing.

Familiarize Yourself With The CC Processing World

Accessing credit card networks isn’t free, hence the reason for processing fees. But, there are many stakeholders involved that want a piece of that sweet processing fee pie.

Before we get into divvying the pie, these are some terms you should know:

- Issuing Banks: The financial institutions, like Chase and Capital One, that issue credit and debit cards to people. Issuing Banks receive the lion’s share of the processing fees.

- Card Networks: Organizations that set interchange rates, determine the rules, and provide the infrastructure to settle payments between banks are the card networks. These are also known as “associations” and “brands” and familiar examples include Visa, Mastercard, and Discover.

- Interchange: The portion of the processing cost that is paid to the Issuing Bank, typically consisting of a percentage of the transaction amount plus a flat fee. These amounts are set by the Card Networks and vary by card type.

- Network Fees: The portion of the processing cost that’s paid to the Card Network. These fees are determined by the network and include “assessments” and per transaction fees.

- Acquiring Banks: Financial institutions that process payments for merchants and settle funds to the merchant accounts. They’re also known as merchant banks.

- Credit Cards: Payment cards issued to cardholders offering a line of credit that can be used to make purchases, and cardholders are then required to pay back the loan amount. Credit cards have significantly higher interchange rates than debit cards.

- Debit Cards: Payment cards that deduct funds that already exist in consumer accounts. “Signature debit” cards are processed in the same manner as credit cards (no PIN required), but have much lower interchange rates than debit cards. 45% of food and beverage industry transactions are debit!

If your eyes are going cross, don’t worry! Visuals and tangible examples are coming.

Let’s Dive Deeper On Interchange

Interchange plays a large part in your business’s profitability, and therefore in determining the best POS processing fee structure for you.

Interchange is the pass-through cost set by Card Networks and Issuing Banks. It varies based on a guest’s card brand (Visa/Amex), type (debit/credit/rewards), and transaction type (keyed/swiped), and it’s impossible to perfectly predict ahead of time. It’s also non-negotiable, and every merchant that accepts card payments pays these fees.

This equation is how POS providers determine processing fees:

Interchange Plus = Interchange Rate + % of transaction + transaction fee

Because Interchange Rate is dependent on the transaction, you should keep an eye on the last two numbers (percent of transaction and transaction fee) when comparing POS processing rates.

Comparing Interchange Plus & Flat Rate Processing

Choosing a POS payment processing fee structure is an important decision because of its affect on your business’s profitability. In fact, whether you make money on payment processing or not depends on two distinct factors:

- Whether you choose an Interchange Plus or Flat Rate fee structure

- Your business’s percentage of credit vs. debit cards transactions (Keep in mind 45% debit is standard for the food and beverage industry.)

Because debit cards have significantly lower interchange rates than credit cards, those transactions cost less to process. So who saves when a debit card is swiped (or dipped or tapped)?

- The Interchange Plus fee structure passes debit savings onto you

- The Flat Rate fee structure passes debit savings onto the POS provider

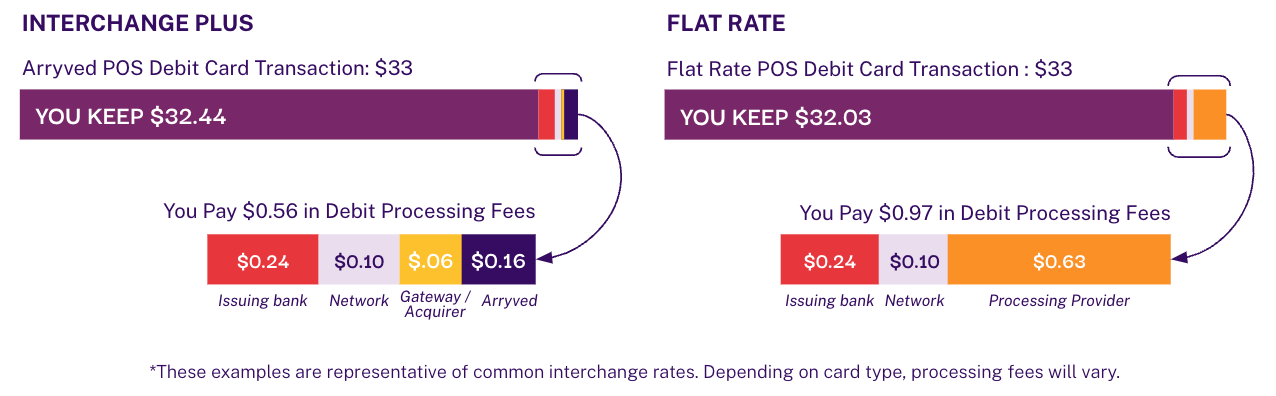

This is a real example comparing two debit transactions using Arryved POS (with an Interchange Plus fee structure) versus a POS provider with a Flat Rate fee structure.

As you can see, Interchange Plus saves you 41 cents as compared to Flat Rate. That small change adds up over time when you consider that nearly half of your guest transactions are debit!

Interchange Plus Is The Most Profit-Friendly POS Fee Structure

Interchange Plus is the fee structure that charges the true pass-through cost for all card types, meaning cheaper debit processing and higher growth potential for your business.

Arryved POS uses Interchange Plus processing, which saves you money on every debit transaction. Plus, Arryved offers many other benefits to small businesses in the food and beverage industry:

- Industry Expertise: Arryved’s team is stacked with industry veterans and hospitality gurus that genuinely want to help your business grow. They’ve been in your exact shoes before, and can better advise, train, and educate you on best practices in the industry. Plus, they’re really fun to work with!

- Specialized POS System: Arryved’s system goes beyond payment processing to provide a seamless service experience, making your staff’s jobs easier and your guests happier. Arryved features prioritize mobility and flexibility, and the sophisticated tool set evolves as your business does, so you’ll never be held back by technology again.

- Educational Resources: Arryved builds partnerships on trust and transparency. Access on-demand resources such as webinars, how-to guides, and blogs like this one so you can make informed business decisions.

Request a free, custom demo with a Growth Specialist today to see how Arryved’s fee structure and product suite increase your bottom line.